In Part 1 of our Mid-Market Hotels Series, we identified the strategic stasis of the current market; the second chapter is being written for the P&Ls. As travel patterns flatten for the economy and some lower‑midscale brands, a “K‑shaped” reality has emerged. True mid‑market assets in attractive locations are proving to be the industry’s Goldilocks zone -capturing the migration of travelers moving down from upper‑tier properties, where the experience lines have now blurred for value, and up from economy for more consistent quality.

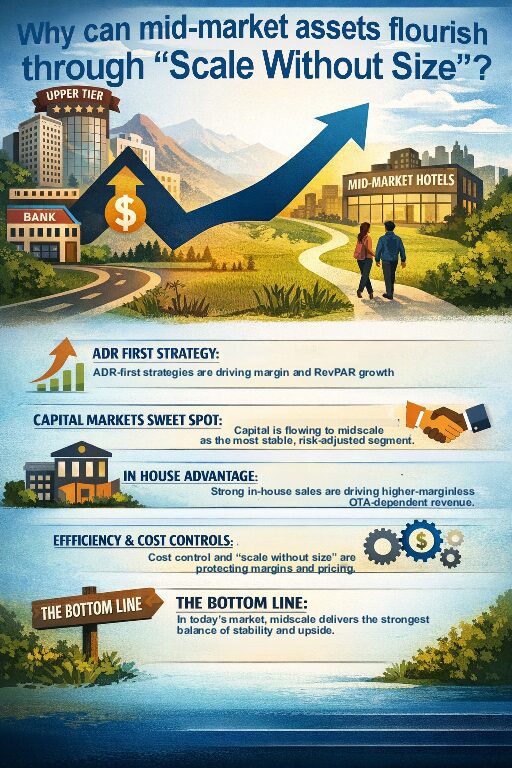

An ADR‑First Strategy: In an era of elevated operating expenses, occupancy is no longer the primary trophy. We are seeing sophisticated owners move away from heads in beds at any cost, instead utilizing AI‑driven revenue management to prioritize ADR‑driven profitability and market penetration. By leaning into brand‑direct booking channels and reducing OTA dependency, midscale owners are reclaiming 300–500 basis points of margin that previously leaked out to third‑party commissions, allowing them to outpace their comp sets in RevPAR growth. This has been an emerging pattern for some time but has recently become an invaluable strength of well‑run midscale assets.

Capital Markets & The Firm Middle Ground: The current lending environment has significantly challenged the assumptions of the post‑COVID boom, but the mid‑market remains a preferred destination for debt. Because these assets offer a “floor” of consistent brand‑driven demand and a “ceiling” of lower operational overhead, they are being underwritten as the most resilient risk‑adjusted play in 2026. For investors, this translates to a lower entry burden; lenders are offering more favorable debt‑service coverage ratios and higher LTVs for midscale flags compared to, say, higher‑risk secondary‑market boutiques or struggling economy tiers.

The In‑House Advantage: Our buyers are increasingly weighing the strength of an asset’s local sales engine, or at least its independent ability to capture local demand and share-rather than strictly relying on brand and OTA contribution. Properties that complement the brand’s global topline with a dedicated in‑house sales effort are successfully capturing high‑yield corporate accounts – and reducing reliance on the often higher‑cost brand‑ and OTA‑driven revenues. This base business allows for a more aggressive retail rate strategy during peak periods, effectively insulating the assets from the recently seen cooling leisure demand in lower tiers.

The Efficiency Story: When we underwrite a listing in 2026, we are looking for its margin durability. With projections tightening due to instability in the driving factors, the market is placing a premium on assets that have optimized their cost controls for better flow‑through. However, the unique advantage of this segment is the “Scale Without Size” factor, or its ability to leverage things like procurement and vendor contracts to contain costs on everything from linens to LVT flooring. This franchise‑backed negotiating leverage, combined with leaner‑than‑upper‑tier staffing models, allows midscale assets to command higher market pricing by proving they can protect cap rates with stabilized revenues, even in inflationary cycles.

The Bottom Line: The narrative has shifted from “waiting for rates to drop” to “working the available capital stack.” In a market where cost controls and capital access are the primary hurdles, the midscale and upper‑midscale segments offer the perfect blend of brand‑driven revenue and operational flexibility. Whether you are navigating a scenario with a net‑positive picture for exit equity or are looking to underwrite a new acquisition to these high‑performance parameters, our team of market professionals is ready to assist you in securing your next move.

Contributed by Matt Lawrence